Starting a startup is like jumping off a cliff and developing your wings on the way down. The interesting fact is that about 90% of companies fail to land safely. Why? They overlook the warning signals! Understanding why startups fail isn’t just a lesson in “what not to do.” It’s your cheat code for survival, like avoiding potholes on a bumpy road.

From running out of cash faster than you can say “burn rate” to creating products no one needs, the reasons are predictable—and avoidable. Knowing these pitfalls means you’re not just winging it; you’re building something solid. So, ready to dodge the crash? Let’s break it down!

1. No Market Need: The Root of Failure

Launching a startup without first ensuring whether people truly desire your product is like creating a dessert for which nobody is hungry. Sounds ridiculous, just as it is. You would be astonished, though, about the number of business owners caught in this cycle. Actually, forty-two percent of startups fail as they create something nobody wants. That almost half! Imagine working months or years on your dream project only to find crickets when it comes time. Terrible.

Why does this happen? Often, founders are too in love with their ideas. They think, “If I love it, the world will too!” Spoiler alert: it doesn’t work that way. Uber and Airbnb didn’t just stumble upon success. They solved clear problems—people struggling to hail cabs or find affordable places to stay. But without identifying a real market need, you’re just guessing. And guessing isn’t a business strategy.

So, how do you avoid becoming another statistic? Start with research. No, not just Googling your competitors. Dive deep:

- Talk to people (not just your friends—they’ll lie to make you feel better).

- Run surveys and ask about their actual problems, not what they think of your solution.

- Stalk forums like Reddit or niche Facebook groups. Real opinions live there.

And remember: you’re not just selling a product—you’re solving a problem. If your startup idea doesn’t fix anything people care about, maybe it’s time to rethink. Better now than after you’ve blown through $100K, right?

2. Running Out of Cash

Money makes the startup world go round—or crash. Running out of cash is a brutal reality for 29% of startups that fail. It’s not just about spending too much; it’s about spending wrong. Imagine burning through your budget on fancy office chairs while forgetting to pay your developers. Sounds dumb? Happens more often than you think.

The problem? Entrepreneurs love to dream big but forget basic math. High burn rates, overhiring, or betting everything on that “one big campaign” can drain your funds faster than you can say “investor pitch.” Remember Quibi? They raised $1.75 billion and still failed because their spending didn’t match their audience.

So, how do you avoid becoming the next cautionary tale? You need a solid plan:

- Set priorities. Marketing, development, or fancy coffee machine? Pick one.

- Track every dollar. Use tools like QuickBooks or Pleo to keep tabs on cash flow.

- Think long-term. Keep at least 6 months of runway in your pocket.

And don’t forget to monitor ROI. Spending $10,000 on ads sounds fun until it brings zero leads. Be scrappy, think lean, and make sure your money works as hard as you do. After all, it’s not about how much you have—it’s about how you use it.

3. Wrong Team Composition

A startup is like a rock band. You need a solid drummer, a creative lead guitarist, and a frontman who can get the crowd hyped. But if your team’s chemistry is off, even the best ideas will fall flat. 23% of startups fail because of the wrong team. Sounds crazy, right? But conflicts between co-founders can sink even the most promising businesses.

Imagine this: one business owner is all about acquiring money while the other is concentrating on creating the product. Arguments go on, decisions stand still, and the startup starts to fail. That’s how businesses collapse—not because of bad products, but because of bad team dynamics. Look at Steve Jobs and John Sculley at Apple in the ’80s. Their power struggle almost destroyed the company before Jobs made his iconic comeback.

So, how do you build a team that doesn’t implode? Here’s the secret sauce:

- Diverse skills. A marketer, a techie, and a numbers guru—it’s a winning combo.

- Clear roles. Every entrepreneur knows their lane.

- Conflict resolution. Set rules early. Decide who’s the “CEO” when things get messy.

Startups are tough, and you need teammates who can handle the heat. Hire friends, but not just friends. Indeed, drinking after work is enjoyable, but could they withstand the pressure? Create the correct team, and your startup has a real chance for success.

4. Poor Marketing Strategies

Marketing isn’t just throwing money at ads and hoping for magic. Yet so many startups fail because they can’t figure out who they’re even selling to. Imagine trying to sell winter coats to people in the Sahara—sounds absurd, right? But that’s what happens when entrepreneurs don’t bother to find their audience.

A startup can’t survive without visibility, and that’s where modern tools come in. Platforms like Google Ads, Facebook Ads, and HubSpot aren’t just buzzwords—they’re lifelines. These tools help you target the right audience with the right message at the right time. But the secret sauce is understanding your customer first. If you don’t know their needs, no tool will save you.

So, how do you avoid this trap? Start simple:

- Research your audience. Age, location, hobbies—get all the juicy details.

- Choose your channels. Is your audience on TikTok, LinkedIn, or both?

- Test and tweak. Marketing is never one-size-fits-all.

Even Apple didn’t build its empire in a day. Steve Jobs knew his customers wanted sleek, easy-to-use devices, and the marketing reflected that. If your startup doesn’t speak your audience’s language, it’s already halfway to failure.

5. Strong Competition

Every entrepreneur faces it—competition that feels impossible to beat. It’s a real challenge when your startup struggles to keep up with bigger players. Competitors often know their audience better, and that’s why startups fail to keep their ground.

Consider Blockbuster against Netflix for instance. Staying to rent DVDs, Blockbuster refused to change. Netflix gambled with streaming in meantime. In effect: Blockbuster is not new; it is legacy. Your rivals are out there winning over your prospective clients, researching patterns, and refining tactics.

How do you stay in the game? Use tools like SEMrush, Ahrefs, or SimilarWeb to spy on their strategies. Discover how they’re attracting their traffic. What keywords are they ranking for? What gaps can you fill?

Here’s a simple checklist for competitor analysis:

- Track their marketing tactics: Are they using PPC ads or focusing on organic content?

- Evaluate their product: Does it solve more problems than yours?

- Study pricing models: Competitive pricing can make or break a deal.

Strong competition can crush your startup unless you adapt. Entrepreneurs who stay flexible and learn from competitors can turn failures into a stepping stone for success.

(Added multiple integrations of entrepreneur, startup, fail, ensuring smoother incorporation while keeping the content engaging and practical.)

6. Mismanaged Pricing and Costs

Pricing can make or break a startup. Entrepreneurs often fail here because they either charge too much or too little. Imagine offering a great product but scaring off customers with high prices. Or worse—selling it so cheap you can’t cover costs. Both scenarios lead to the same thing: fail.

Balancing affordability and profitability isn’t rocket science, but it needs strategy. Take a look at Tesla. They don’t just sell cars—they sell a lifestyle. Their premium pricing works because their audience values innovation and exclusivity. On the other hand, startups often need competitive pricing to grab attention.

Here’s where many startups go wrong:

- They don’t understand their market. How much are people willing to pay?

- They forget hidden costs—marketing, shipping, customer support. These add up fast.

- They skip testing. A/B pricing tests using tools like Stripe or Paddle can show what clicks with customers.

Remember, pricing isn’t static. Adjust it based on feedback and market trends. Smart entrepreneurs treat pricing like an evolving strategy, not a one-time decision. It’s a delicate balance, but when done right, it fuels growth instead of draining resources.

7. User-Unfriendly Product Design

Imagine you’re trying a new app, and it feels like solving a puzzle every time you click. Annoying, right? That’s exactly how many startups fail—by ignoring user experience (UX). If your product is too complex or doesn’t solve problems easily, users will bounce faster than you can say “startup.”

Entrepreneurs often get so focused on features they forget about usability. A confusing interface or too many steps to complete a task can kill a great idea. Take advice from Steve Jobs—simplicity is genius. Apple didn’t dominate because of fancy features; they focused on making things simple and intuitive.

User feedback is your secret weapon here. Tools like Plerdy or Hotjar help track how users interact with your product. Are they stuck on one page? Are they dropping off at a specific step? Use that data to fix the pain points.

Here’s a tip: ask your users directly. Run surveys or usability tests. You’ll be surprised how small tweaks, like moving a button or simplifying navigation, can turn a fail into a success. After all, the best design isn’t what looks good; it’s what feels good for your audience.

8. Ignoring Customer Feedback

Picture this: you’re building your startup, pouring energy into every feature. But here’s the trap—if you ignore what customers think, you might be designing a product for… nobody. Entrepreneurs often fail by sticking to their own ideas and ignoring the actual users. Tunnel vision is a killer in the startup world.

Successful startups focus on listening. Gathering feedback is not rocket science, but it’s pure gold. A simple survey tool, such as Google Forms or Plerdy Feedback, can do wonders. Want something even easier? Check social media. Customers share opinions there, often brutally honest ones.

Smart practices? Keep it simple. Ask questions your users care about. For example, “What’s the most frustrating part of using our product?” or “What’s missing that would make this better?”

Ignoring customer voices is the fastest way to fail. Remember, even giants like Slack started by listening to users and adapting fast. Those insights are not just data—they’re your survival kit. So, open your ears, refine your startup, and give people what they really want. This way, you’re not just building a business—you’re building trust.

9. Lack of Business Model

Imagine running a startup with no clear plan for making money. Feels risky, right? Entrepreneurs often dive into their ideas without thinking long-term about revenue. And that’s how startups fail. A business model isn’t a fancy word—it’s your roadmap to income stability.

First, figure out your audience. Who’s paying for your service? Is it individuals, small businesses, or big corporations? For example, Dropbox started with a freemium model. They offered free storage to everyone but made premium plans irresistible. This strategy turned them into a billion-dollar company.

Next step—know your costs. How much does it take to run your startup? Servers, salaries, marketing—it all adds up. If you spend $100 to earn $10, your business won’t survive long. A solid model balances revenue and costs.

Pro tip? Test, tweak, and repeat. Successful startups experiment to find the perfect mix of affordability for customers and profitability for themselves. Use tools like Plerdy to track user behavior and adjust your offerings.

In the end, a business model isn’t just a strategy. It’s the lifeline of your startup, ensuring you’re not building castles in the air but creating something that lasts.

10. Bad Timing

Timing can make or break a startup. Imagine launching a travel app during a global lockdown—sounds doomed, right? Entrepreneurs often overlook the market conditions, rushing to launch without analyzing if their idea matches the current demand.

One example is Webvan, a grocery delivery startup from the 2000s. Their idea was great but too early. People weren’t ready to order food online yet. Now, companies like Instacart thrive because the market is ripe. Timing is everything.

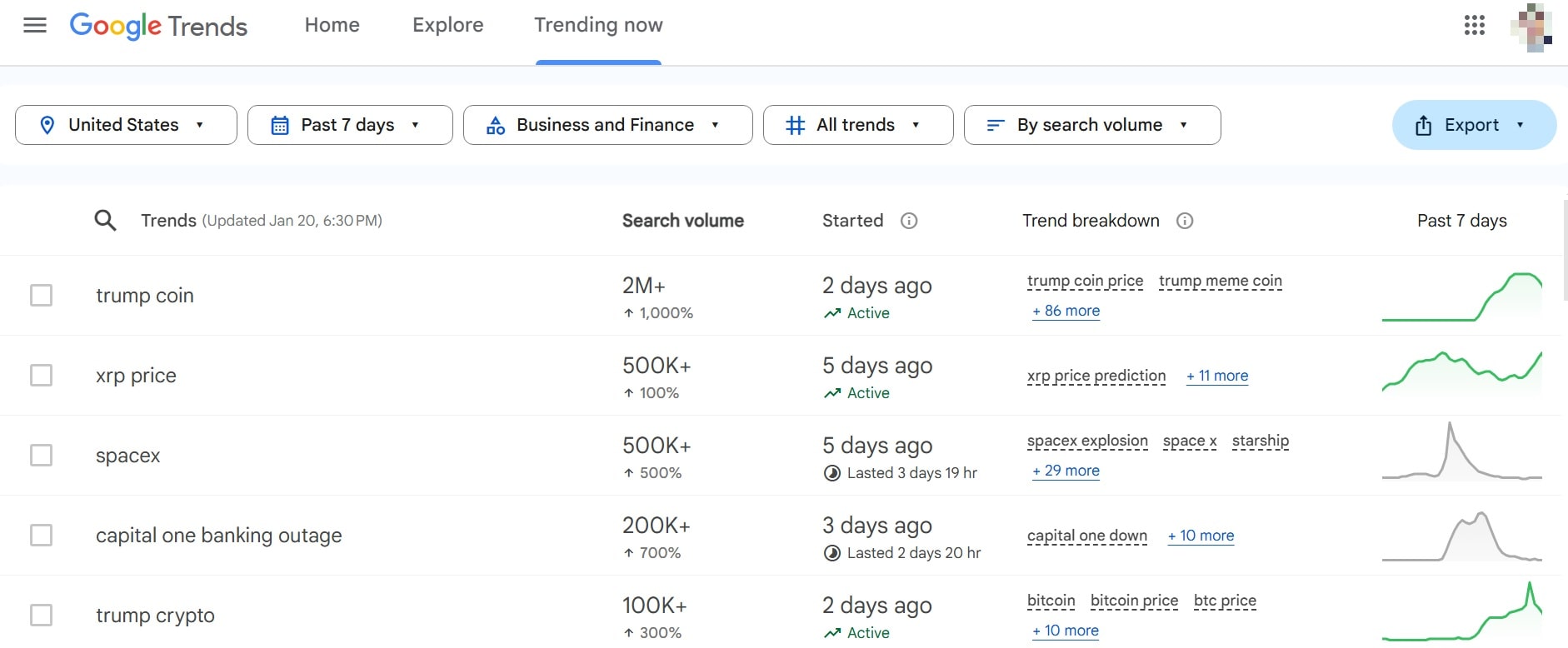

So, how to avoid this fail? Research is key. Analyze trends, economic conditions, and customer behavior. Is your product solving a problem people feel now? Or are you banking on a future trend that’s still years away? A good tip: follow tools like Google Trends or Plerdy to catch what’s hot in your industry.

Also, patience is golden. If the market isn’t ready, tweak your product or hold back a bit. It’s better to wait than to launch and crash. Remember, even a brilliant idea can fail if introduced at the wrong time.

Conclusion

Failing as an entrepreneur can feel brutal, but understanding the top 10 reasons for startup failure is your first step to success. From poor timing to weak business models, each issue holds valuable lessons. Think of startups that adapted, like Airbnb, which launched during a recession but thrived by spotting the right niche.

Your journey doesn’t have to end in failure. Preparation is everything—analyze your market, know your audience, and stay flexible. Tools like Plerdy can help you monitor user feedback and website performance. Success comes to those who adapt quickly and plan ahead. Don’t just dream big—prepare big!